April 2021 — Climate Bonds released the Sustainable Debt-Global State of the Market report, which assesses the scale and depth of the green, social, and sustainability (GSS) debt markets as of the end of 2020.

This report is the tenth iteration in our flagship State of the Market series, encompassing established green markets and the expanding social and sustainability labels.

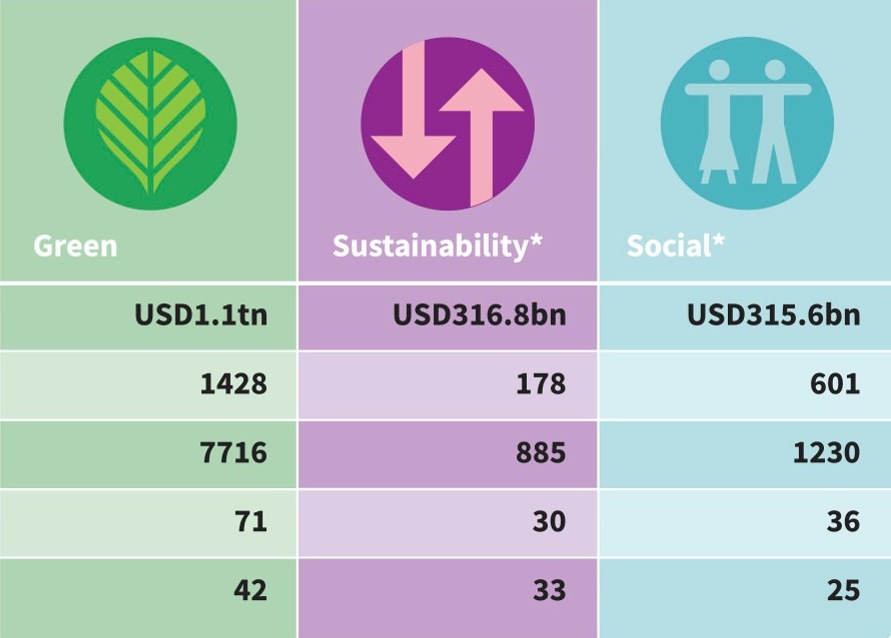

The market analysis examines the changes in the GSS debt markets during 2020, while the forward-looking spotlight section explores the development of transition, green recovery finance and EU green market leadership, three themes that will continue to influence market growth into the 2020s. Read the report.